Owing the government basically means that your total income exceeds your eligible expenses and tax already paid. Taxable income is the portion of your income that the government can tax. You read that right, not all your income is typically taxable. This is because the government understands that some expenses are incurred for income to be earned. These expenses are referred to as eligible expenses. As an employee, these expenses are limited to what your employer permits you to deduct, mainly because every other resource needed to complete your job has been provided. Certain expenses are, however, permitted by the CRA. An example of such an expense is the cost incurred when moving from one point to another for employment purposes. You can read about these in detail here.

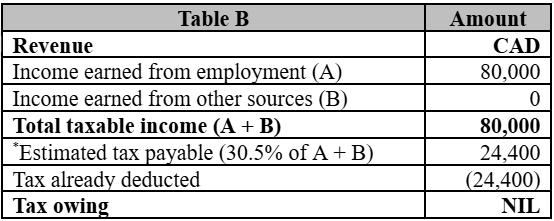

If David worked with TaxWhiz from January 1 to December 31, 2024, earning a gross pay of CAD 80,000 with a total of CAD 24,400 deducted as taxes, David’s taxable income will be CAD 80,000 even though he only took home CAD 55,600 (CAD 80,000 less CAD 24,400) cumulatively during the year.

However, when David is filing his taxes, the CAD 24,400 already deducted as taxes will be factored in, bringing his taxable income to zero – this is with the assumption that his employer deducted the right amount of taxes, and David has no other income to declare or expenses to deduct.